Project Finance vs. Corporate Finance; An investment opportunity in the Renewable Energy Projects

Project Finance vs. Corporate Finance; An investment opportunity in the Renewable Energy Projects

A constructive renewable Energy company may decided to deal with project finance and not corporate finance in a long-term investment for renewable energy projects for multiple reasons in the earlier stage of it’s exploration.

This scenario defines “Project Finance” is seen as enablement to the sponsors to maintain distribute capital towards a long term investment in the renewable energy projects

Havelet Finance Limited is a channel Island private lender. We offer an international project finance in developing projects within the spheres of solar, wind, biomass, waste-to-energy, hydropower, energy efficiency, and energy storage projects. We take up your project from the early stage and give them a 100% financing to the end.

How developers Finance Projects

A developer who wants to venture to finance projects for a large constructions of renewable energy project. The developer may willful explore different options. This is done via

1} Project Finance: Developers looks primarily to the revenues generated by a single project, both as the source of repayment and as security for the exposure.

2} Corporate Finance: Secure equity or debt financing at the development company level and then finance the development or construction of the project on its balance sheet.

Project Finance can be referred to Project finance is a specific mode of financing where an SPV (Special Purpose Vehicle) is created by the sponsors for the sole purpose of the project and the financing to the SPV is repaid through the cash-flow generated by the project. Corporations can use Green bonds to raise money to finance projects. The development company more often issues green bonds, but the Asset Holding company can also issue them.

The typical equity/debt ratio used for Project Finance is much higher than for Corporate finance.

In Europe, Solar or Wind project can be up to 90–95% debt-financed. The typical range for the debt-to-equity ratio in a project company is 50% to 95%.

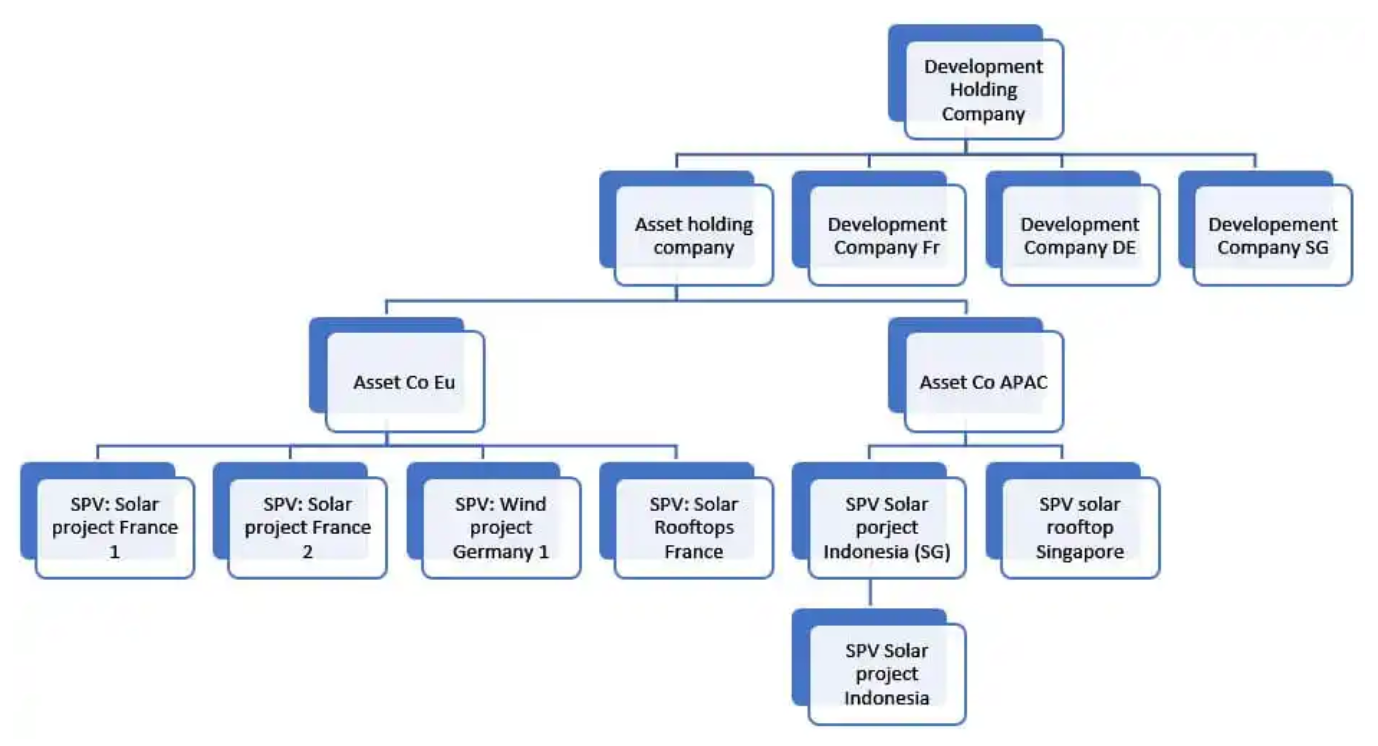

A Typical Asset Structure for Project Finance

A typical asset structure Large projects is vastly associated with SPV. A very essential practices in project finance that introduce debt for a large project from a traditional bank. All project finance succeeds within the spheres of SPV . Nevertheless, it is common that investors request a specific investor and tax-friendly jurisdiction for the SPV used to inject the investment.

A micro projects can be substantiate in a single SPE. Nevertheless, it is important to ensure that the projects included in an SPV share the same risk and return profile to make the debt project financing possible and fair. It is common to group small Solar rooftop projects in a single SPV.

A developer may also group solar rooftop projects based on some criteria as Off-taker credit risk and Off-take agreement type.

Development Corporate Structure

Project Finance vs. Corporate Finance

Project finance reduces the risk associated with the sponsoring firm as compared to corporate finance, this is because the lender solely depends only on the project revenue to repay the loan and cannot pursue the sponsoring company’s assets in the case of default. However, a sponsoring company can only use project finance where it can demonstrate that revenue streams from the completed project will be sufficient to repay the loan.

For any project finance chronicles, the investor is obligatory to discharge or implement the following approaches;

- Identify and evaluate risks

- Define the pricing

- Structure the deal and associated collaterals/guarantees

- Evaluate impacts

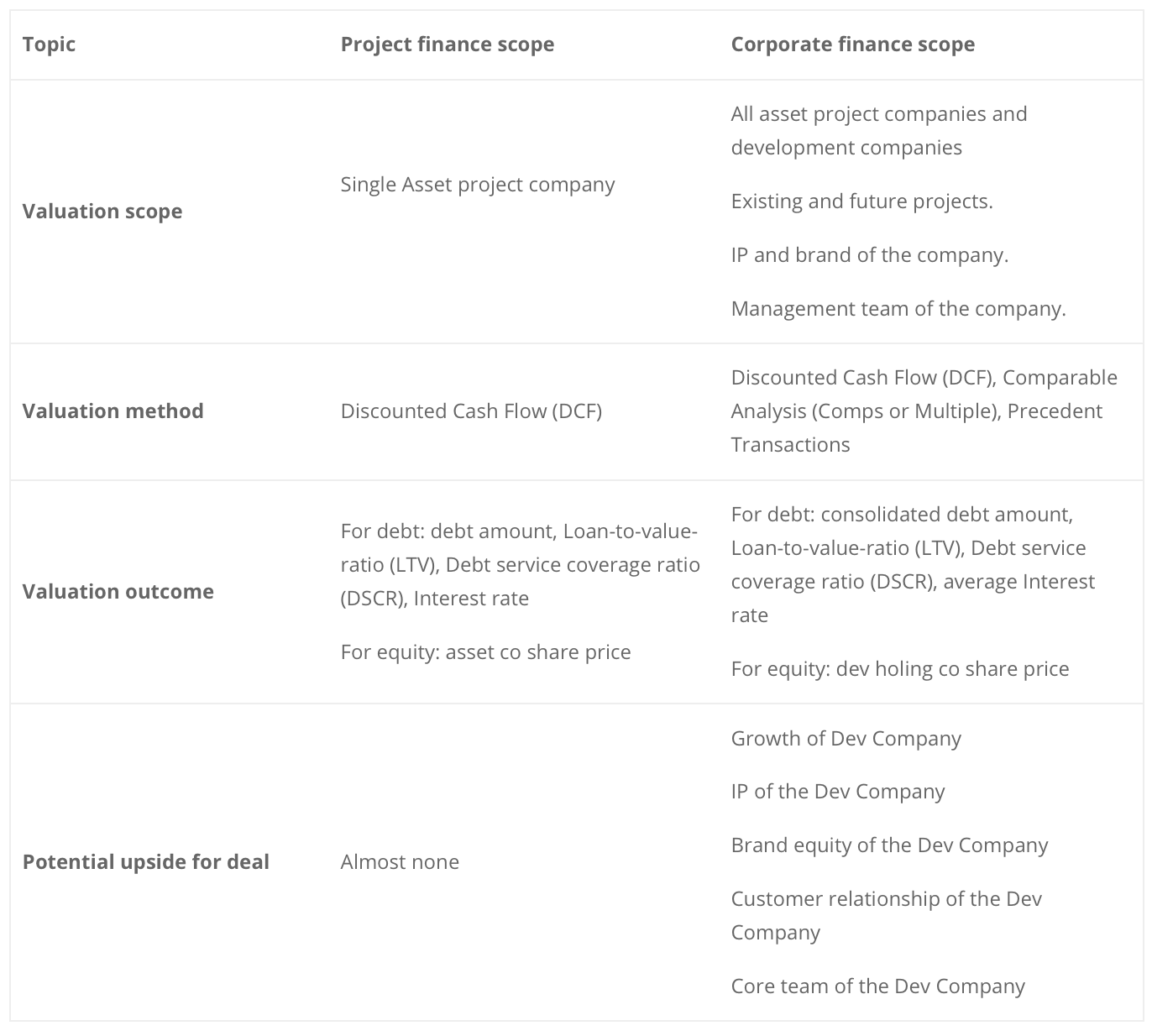

Depending on the type of financing used, the work will be different. comparing the different between corporate vs. project financing.

Risks assessment: The entanglement to evaluate risk comprises of higher investment at the corporate level than at the project level. When investing at the corporate level, it is common for investors to ensure that the development company will use similar contracts and agreements to limit variability in the risk profiles.

Pricing: Negotiation and bargaining or pricing the asset to purchase is paramount by the investor. A lender will also need to scrutinize the financial base that would shape the debt financing effectively and understand the risk profile to define the correct premium. The scope of the assessment will be different for project financing or corporate financing. The diagram below defines the above mentioned

The Layout of collaterals/guarantees for Project Finance and Corporate Finance

Projects finance is associated with high-risk, capital intensive, and time-consuming in nature. Hence, the project finance model requires special skills and techniques, given the nature of project work. In this type of model, capital is infused into projects based on its forecasted cash flow, which along with the project assets

in corporate finance, the lenders is in power to allege the assets belonging to the parent company’s assets. Basically, if a company announces its bankruptcy, then the lenders can seize the borrower company’s assets and auction to recover their debts. On the other hand, the project in project finance is ring-fenced from the sponsoring company. Basically, a special purpose vehicle is created for the project-related transactions, and the lenders’ claims are only limited to the cash flows of the special purpose vehicle.

The evaluation of the impact of the invested funds is simpler and more accurate at the project level than at the corporate level. There is also less overhead included in the financing. Indeed, project finance is an effective way to control the usage of funds. The funds can be made available step-by-step according to the project development and construction progress. By doing so, the impact investors can maximize their impact per capital deployed. They can also be more selective in the types of projects they support.

The Benefits of Project Finance

In order to clarify the implementation of deals and manage their asset portfolio, we recommend that impact investors invest at the project level and not the corporate level.

We recommend that investors use similar approach/structuring as a bank when providing debt project financing. But impact investors can bring additional values than banks to the project. For example, investors can be faster in making investment decisions, accept to come earlier into the project lifecycle, support more impactful or innovative projects, be more flexible with the credit assessment of the project sponsor.

Traditional Corporate Finance oversees the securities inline with can offer equity investors as all the underlying assets of the development company can be used as collateral. To compensate for this, project equity investors can use — if necessary — warrants (at the corporate level) to ensure that they will be compensated in case of a default event at a single project levels.

Disadvantages of Project Finance

Project finance do not have expensive resources under all circumstances and in all ventures, hence the contracting expenses are still very high.

Complexity: The funding of the project is based on a series of contracts involving agreements with all project participants. Negotiations themselves can be very complicated and often costly to carry out.

Indirect Credit support: The loan cost is higher for all the lenders without exception, resulting from indirect credit assistance.

Higher Transition costs: It needs higher funding costs relative to those incurred indirect financing because of its complexity. It represents the contractual costs in the design of the financial framework of the project.

Havelet Finance Limited offers the following;

• Long-term loans for up to 20 years.

• Organization of project finance (PF) schemes.

• Operations with letters of credit or bank guarantees.

• Financial modeling and consulting.

• Investment engineering.

Website: https://www.havelet-finance.com

Email: credit@havelet-finance.com

Comments

Post a Comment